Loan for tax arrears

Unexpected tax bill? A loan can help. Check your options now and secure a tailored financing solution.

Published on

Last updated on

4 min read

Table of Contents

Loan for paying tax arrears: How to finance claims from the tax office

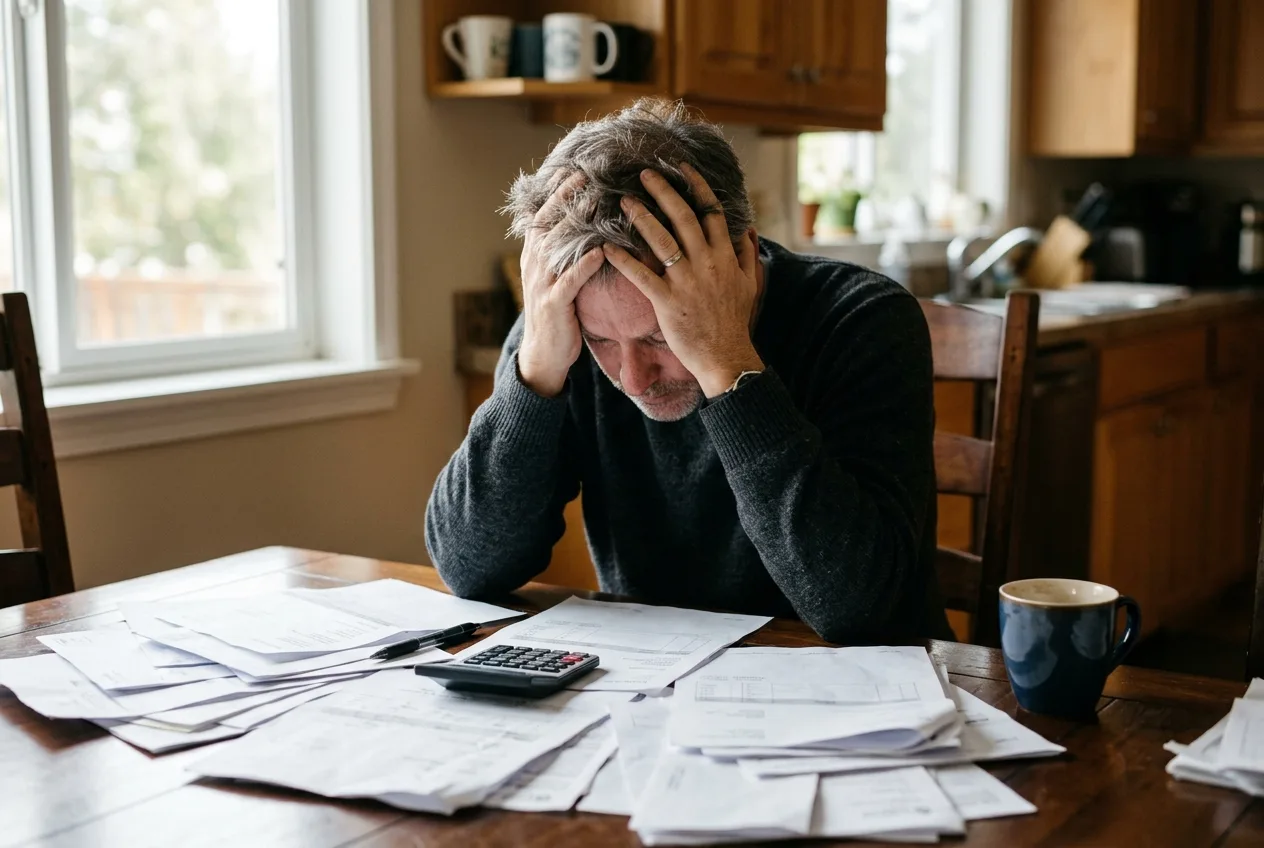

Does your tax assessment bring a large back payment and present you with financial challenges? This is a stressful situation for many self-employed people and employees, but there are effective solutions. A targeted loan can not only ensure payment on time, but is often cheaper than the interest and penalties charged by the tax office.

Understanding the causes and consequences of high tax back payments

A large tax bill can arise for many reasons, for example due to additional income, an unfavourable choice of tax class for married couples, or received wage replacement benefits such as short-time working allowance of more than €410. For the self-employed, it often results from a financial year that performed better than expected. The consequences of a late payment are severe. The tax office charges late payment penalties of one per cent for each started month of delay on the rounded tax debt. With a tax debt of €5,300, this can quickly lead to noticeable additional costs. Unpaid tax debts can also negatively affect creditworthiness and make future financing more difficult. In the worst case, the authority will initiate enforcement measures such as an account garnishment to recover the claim. To avoid these costly and unpleasant consequences, prompt action is crucial.

The instalment loan as a strategic solution for tax debts

An instalment loan is often the quickest and most economically sensible solution for settling a tax arrears payment. The interest on a consumer loan is often lower than the six per cent annual interest charged for a deferment by the tax office or the twelve per cent charged in late payment surcharges. A loan provides immediate liquidity, so you can settle the debt on time and avoid all further fees. In addition, a loan for any purpose offers maximum flexibility. The clear monthly instalments of a loan allow better financial planning than an uncertain deferment agreement. Thanks to digital processes, applying for a loan today is possible online in just a few steps. This gives you a decisive time advantage over lengthy negotiations with the tax authority.

Alternatives to a bank loan: deferral and instalment payments with the tax office

Before taking out a loan, you should check the options directly with the tax office. You can apply for deferral or instalment payments if immediate payment would constitute a “significant hardship”. This applies where your economic livelihood would be at risk. However, the hurdles for this are high, and the tax office examines strictly whether you could not raise the funds in another way, for example through a bank loan. The decision is always at the discretion of the case officer; there is no legal entitlement. In addition, approved deferrals incur interest at 0.5 per cent per month. The following points should be noted when submitting an application:

- The application must be submitted in writing and be well substantiated.

- You must provide evidence of your financial hardship.

- The deferral must not jeopardise the tax claim.

- For certain types of tax such as income tax and VAT, deferral is generally not granted.

A loan often offers more security and better terms than the uncertain commitment from the tax office. A targeted debt consolidation loan can also be an option to bundle expensive liabilities. Negotiating with the authority is therefore one possibility, but rarely the most advantageous.

Step by step to the right loan for your tax bill

Taking out a loan to settle tax debts is a clearly structured process. With good preparation, you can quickly find a suitable financing solution. Carefully preparing a household budget is the first step in determining your financial room for manoeuvre. Digital loan comparisons make it possible to quickly review offers with interest rates between 0.69 per cent and 19.99 per cent. Here’s how to proceed:

- Determine your borrowing requirement: Determine the exact amount of the tax bill plus any buffer for unforeseen expenses.

- Compare offers: Use online comparison portals to review the interest rates, terms and conditions of different banks.

- Submit an application: Complete the loan application digitally and submit the required documents such as proof of income and the tax assessment notice.

- Receive the payout: After successful assessment, the loan amount is often transferred to your account within 24 to 48 hours.

This structured approach helps you keep control of the situation and make an informed decision. A quick loan for unforeseen bills may be a suitable solution here.

Expert tips: proactively avoid future tax back payments

Once the current claim has been settled, you should take precautions to avoid future surprises. Forward-looking financial planning is the key. If your income fluctuates, proactively adjust your tax prepayments to prevent a large shortfall at the end of the year. A conversation with the tax office or a tax adviser can bring clarity here. Our expert tip: set up a monthly standing order of ten to 15 percent of your income into a separate easy-access savings account. This simple measure creates a financial buffer specifically for tax payments. This way, you can ensure that the next tax assessment no longer triggers a financial crisis. If unexpected expenses do arise, the option of increasing an existing loan may also be worth considering.

Conclusion: Maintaining financial sovereignty

An unexpected tax bill is a serious financial burden, but it can be managed with the right strategy. A loan to pay an unexpected tax bill is often the best way to avoid costly late payment penalties and protect your credit rating. While a deferral from the tax office is an alternative, it comes with significant hurdles and an uncertain outcome. By taking proactive measures such as adjusting advance payments and building reserves, you can prevent future additional tax demands. This will help secure your financial stability in the long term. Request an individual risk analysis now: Have your insurance situation reviewed free of charge and receive specific recommendations for improvement.

Frequently asked questions

- Is a loan to pay the tax bill always the best solution?

A loan is often a very good solution for avoiding high late payment penalties (twelve per cent per year). The interest on an instalment loan is usually much lower. However, it is advisable to first ask the tax office directly whether interest-free, short-term instalment payments are possible, even though this is rarely granted.

- What documents do I need for a loan application?

For a loan application, you usually need your identity card, current proof of income (payslips or management accounts for self-employed people) and the tax assessment notice showing the additional payment. Some banks also require bank statements for the last few months.

- Does a loan for tax debts affect my Schufa?

The credit enquiry itself is generally Schufa-neutral. A properly repaid loan can even have a positive effect on your score. Far more damaging for Schufa is an unpaid tax debt that leads to enforcement measures.

- How can I avoid future tax arrears?

Adjust your tax prepayments to your current income. Also set money aside each month, ideally ten to 15 per cent of your income, in a separate account. Regular reviews of your finances with a tax adviser are also helpful.

- What is the difference between deferral and paying by instalments at the tax office?

A deferral postpones the entire payment to a later date. An instalment plan divides the debt into several smaller amounts. Both must be applied for and require „significant hardship“, with the decision resting at the discretion of the tax office.

- How quickly will I receive the money from a loan?

With online loans, assessment and disbursement are often very quick. After all documents have been submitted digitally and a positive assessment has been made, the loan amount can often be in your account within 24 to 48 hours, allowing you to meet the tax office deadline.

Sources

- [1]The Federal Ministry of Finance offers a comprehensive overview of taxation in Germany.

- [2]The Federal Ministry of Finance explains the term “tax offices” and their responsibilities in its glossary.

- [3]The Federal Ministry of Finance defines in its glossary who is considered the taxpayer.

- [4]The Federal Ministry of Finance explains the term “deferral” in tax law in its glossary.